Ways To Locate The Most Effective Home Mortgage Rate

Article by-Dalby PruittAre you curious about what a mortgage is? A mortgage is a long-term loan that is secured by your property. If you are in default of the loan, your house will be repossessed from you. Taking out a mortgage is huge, so the tips below are important to help you through the process correctly.

Hire an attorney to help you understand your mortgage terms. Even those with degrees in accounting can find it difficult to fully understand the terms of a mortgage loan, and just trusting someone's word on what everything means can cause you problems down the line. Get an attorney to look it over and make everything clear.

Try shopping around for a home mortgage. When you do shop around, you need to do more than just compare interest rates. While they're important, you need to consider closing costs, points and the different types of loans. Try getting estimates from a few banks and mortgage brokers before deciding the best combination for your situation.

Consider the Federal Housing Authority to be your first stop when looking for a new mortgage. In most cases, a mortgage with the FHA will mean putting a lot less money down. If you opt for a conventional loan, you will be required to come up with a serious down payment, and that can mean not being able to afford the home you really want.

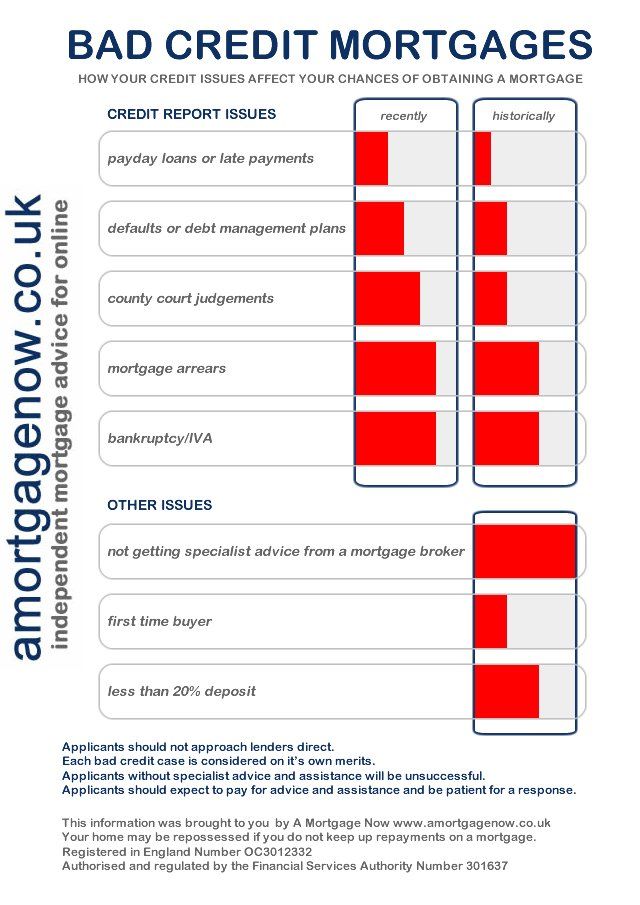

Obtain a credit report. It is important to understand your credit rating before you begin any financial undertaking. Order reports from all 3 of the major credit reporting agencies. Compare them and look for any erroneous information that may appear. Once you have a good understanding of your ratings, you will know what to expect from lenders .

Obtain a credit report. It is important to understand your credit rating before you begin any financial undertaking. Order reports from all 3 of the major credit reporting agencies. Compare them and look for any erroneous information that may appear. Once you have a good understanding of your ratings, you will know what to expect from lenders .

You can request for the seller to pay for certain closing costs. For example, a seller can pay either a percentage of the closing cost or for certain services. Many times the seller is responsible for paying for a termite inspection along with a survey and appraisal of the property.

Try giving your lender a chance to help you with mortgage payment problems. If you struggle to make payments, do not ignore your lender's services. There are various new programs to help you keep up with your mortgage payments like forbearance if you have an FHA mortgage. Lenders are generally happy to work out any delinquent loans via loan modifications, or possibly short sales if you can't afford to keep your home. It can be difficult to deal with them over this, but communication is key.

Try going with a short-term loan. Since interest rates have been around rock bottom lately, short-term loans tend to be more affordable for many borrowers. Anyone with a 30-year mortgage that has a 6% interest rate or higher could possibly refinance into a 15-year or 20-year loan while still keeping their the monthly payments near around what they're already paying. This is an option to consider even if you have slightly higher monthly payments. It can help you pay off the mortgage quicker.

Shop around for the best mortgage terms. Lenders individually set term limits on their loans. By shopping around, you can get a lower interest rate or lower down payment requirements. When shopping around, don't forget about mortgage brokers who have the ability to work with multiple lenders to find you the best rate.

Make sure that you have a good amount of savings before you get yourself into a home mortgage contract. There are not certainties when it comes to the economy or job stability. To protect yourself you want to have enough money saved to make your payments for many months in case the worst does occur.

Look closely at lenders. There are many companies willing to lend you money to finance your home. They are not all equal. Look into the reputation of the lender and try to talk to people who have their loans through them. Reputations are hard to hide, and you will want to know how your potential lender handles business.

Learn about the three main types of home mortgage options. The three choices are a balloon mortgage, a fixed-rate mortgage, and an adjustable-rate mortgage (ARM). https://www.joplinglobe.com/region/national_business/first-republic-bank-board-of-directors-appoints-mike-roffler-as-chief-executive-officer/article_7244b872-8264-57ab-9193-f47a81eb7dde.html of these types of mortgages has different terms and you want to know this information before you make a decision about what is right for you.

If you need to make repairs to your home you may want to consider a second home mortgage. As long as you have a good history of paying on time you should be able to get a great rate, and by improving your home you are increasing its value. Just be sure that you will be able to make the payments.

Most financial institutions want the assurance that the property they finance is insured and the property taxes are current. They do this by requiring that you add an amount to cover those expenses to your mortgage payments. This is called an escrow account, and most people find it is convenient to set up payments this way.

Be aware that certain things may need to be done to the property before the loan can be approved. One such thing is extra insulation added to the home. This work can either be done by the home buyer or the homeowner. However, once the work is completed, it must be inspected by a certified inspector.

Pay at least 20% as a down payment to your home. This will keep you from having to pay PMI (provate mortgage insurance) to your lender. If you pay less than 20%, you very well may be stuck with this additional payment along with your mortgage. It can add hundreds of dollars to your monthly bill.

Get at least three mortgage offers before deciding on which one to go with. Home mortgages, like many other loans, will vary in their costs and rates from lender to lender. What you think is a good deal may not be, so it's important to see multiple options before making a decision.

With the advice that has been given to you, you are now equipped to enter the mortgage market and begin deciding which route you want to take. It's important that you understand all of your options, and you want to feel in control and not thrown into a mortgage by a lender that doesn't fit your needs. Instead, go forth and get the right mortgage!